Where do people go for financial guidance?

21 min read

As more of us use social platforms such as TikTok and YouTube to discover finance expertise, we have researched just how reliable these resources are.

Many of us look for guidance before making financial decisions with the aim of making informed choices when it comes to things like investing, taking out credit cardsopens in a new tab and budgeting our finances. In recent years financial guidance has become even more accessible thanks to social media platforms, which have opened up the world of finance to millions of more people.

At Capital One we believe that credit should be transparent and that everyone should feel confident that they are getting the correct guidance when researching financial products. With more of us trusting social platforms, we decided to take a look at how many people are using social media to get their financial guidance and analyse the quality of the content currently available.

Alongside this, we've done a deep dive into the UK's level of financial literacy researching how many of us have a good level of understanding of key financial terms and uncovering where in the UK people have the highest level of financial literacy.

What we did

We surveyed 2,000 adults representative of the UK population which contained questions on gaining financial guidance and their opinions on guidance on social media or from influencers. We also asked them to complete a financial literacy test to reveal their understanding of key financial terms.

We analysed over 1800 videos on YouTube which discussed key financial terms and keywords to uncover if the guidance being given was of high quality.

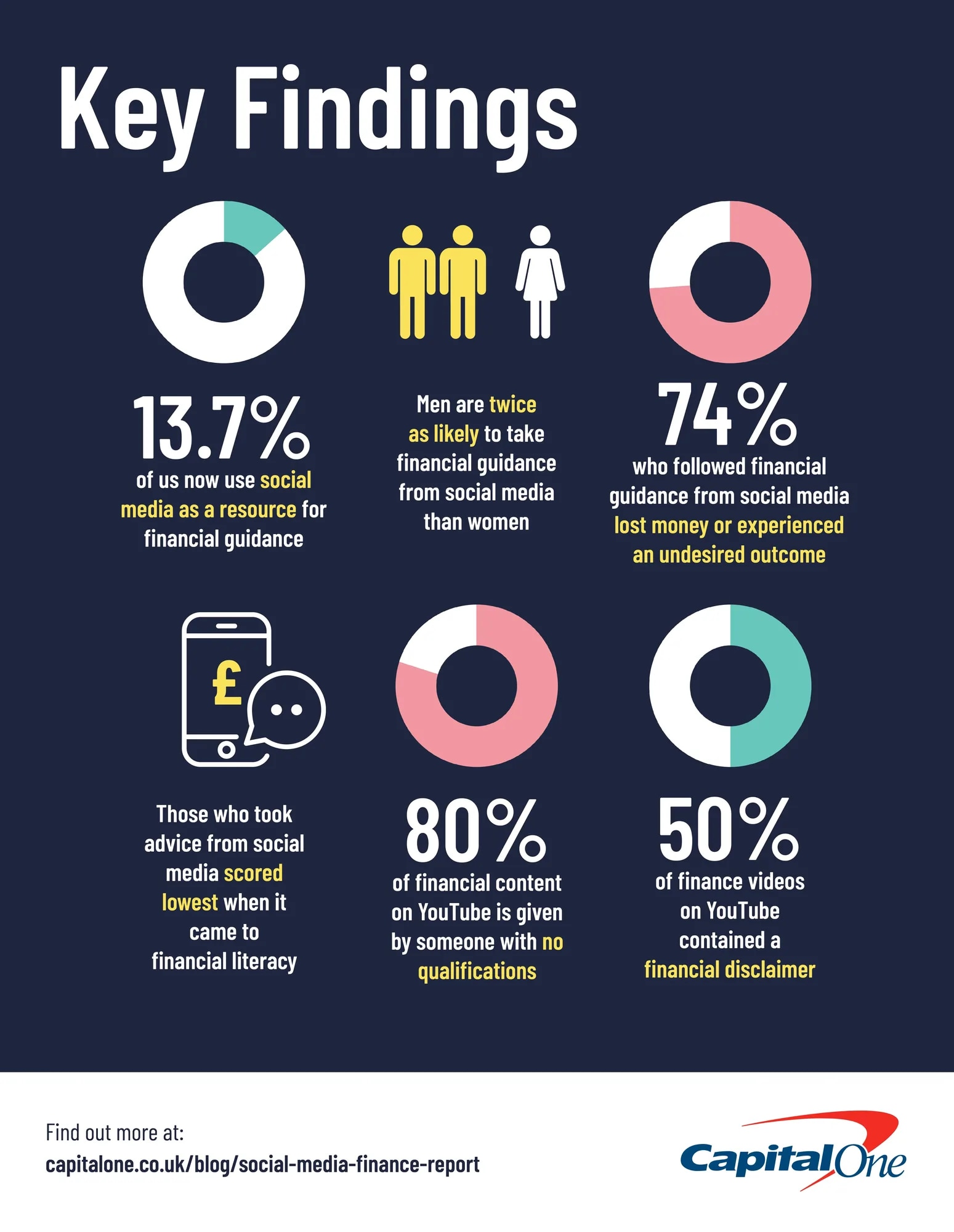

Key Findings

- 13.7% of us now use social media as a resource for financial guidance

- Men are twice as likely to take financial guidance from social media than women

- 74% of those who followed financial guidance from social media lost money or experienced an undesired outcome

- London residents scored lowest on the financial literacy test whilst those living in Yorkshire and the Humber scored the highest

- Those who took guidance from social media scored lowest when it came to financial literacy

- 80% of financial content on YouTube is made by someone with no qualifications

- Only 50% of finance videos on YouTube contained a financial disclaimer

What is financial advice?

Before diving into the findings it's important to understand what we mean when we talk about 'financial advice'. Financial advice is any information given about a specific financial productopens in a new tab it directs you to make a specific financial decision, such as making an investment. Financial advice is regulated and can only be given out by somebody with a relevant financial qualification. This differs from financial guidance, which gives you information about various products and service options which are available. Guidance doesn't steer you to make a specific decision, and as such can be provided by varying individuals or organisations.

Social media as a source of financial guidance

Social media is used widely across the globe. As of 2022, over 4.59 billion people worldwide are using social media, which is projected to increase to almost 6 billion by 2027.1 With its growth, we have also seen a rise in content creators. There is an 'influencer' for pretty much every category now, including finance.

With finance being such a technical topic, it's important for guidance to be accurate. With there being no current regulations around who can post this type of content, is the world of finance influencing something that we can trust? Within this report, we have sought to uncover how many of us are really getting financial information from social media, and how trustworthy it currently is.

How many people use social media to get financial guidance?

The results from our survey revealed that the majority of Brits don't use social media or influencers for financial guidance. In fact, this is the least used source, with just 13.7% of those surveyed admitting that they have got financial guidance from a social media platform or influencer at some point.

Interestingly, traditional banks and financial advisors are the most popular sources, with 25.9% of respondents identifying that this is their primary source of information. With finance being such a complex topic, it's reassuring to see that Brits are mostly approaching experts for guidance.

Men are more than twice as likely to take guidance from social media compared to women

Interestingly, the results revealed that more men than women have taken financial guidance on financial matters from people on a social media platform. 19.6% of males revealed that this was a source that they had used, whereas just 8.1% of females stated that they had used it as a source. This is somewhat unsurprising given that more men cited financial guidance as trustworthy than women (84% vs 79%).

London is where most people take guidance from social media

According to the data, residents of the capital of the UK are the biggest fans of using social media for financial guidance, with 37% citing that they have used it as a source in the past.

Most residents of London are also very trusting of social media for financial tips, with 85% admitting that they found social media platforms trustworthy when looking for this information.

Guidance from social media led to a negative outcome for 74%

Despite most people not using social media to improve their financial knowledge, out of those that have, the experience hasn't been great. In total, nearly 75% of Brits who have made financial decisions based on what they've seen on social media have not received the desired result, e.g. lost money or saw something negatively impact their credit score.

Delving deeper into the data, young men are more likely to lose money from taking guidance from social media than young women. 80% of males ages 18-24 revealed that they have fallen victim to the guidance they have followed from social media, whereas just 28.6% of females from the same age group said they had experienced the same.

Where else do people get financial guidance?

Outside of social media, there are many other places we can absorb financial information, but where are the most popular?

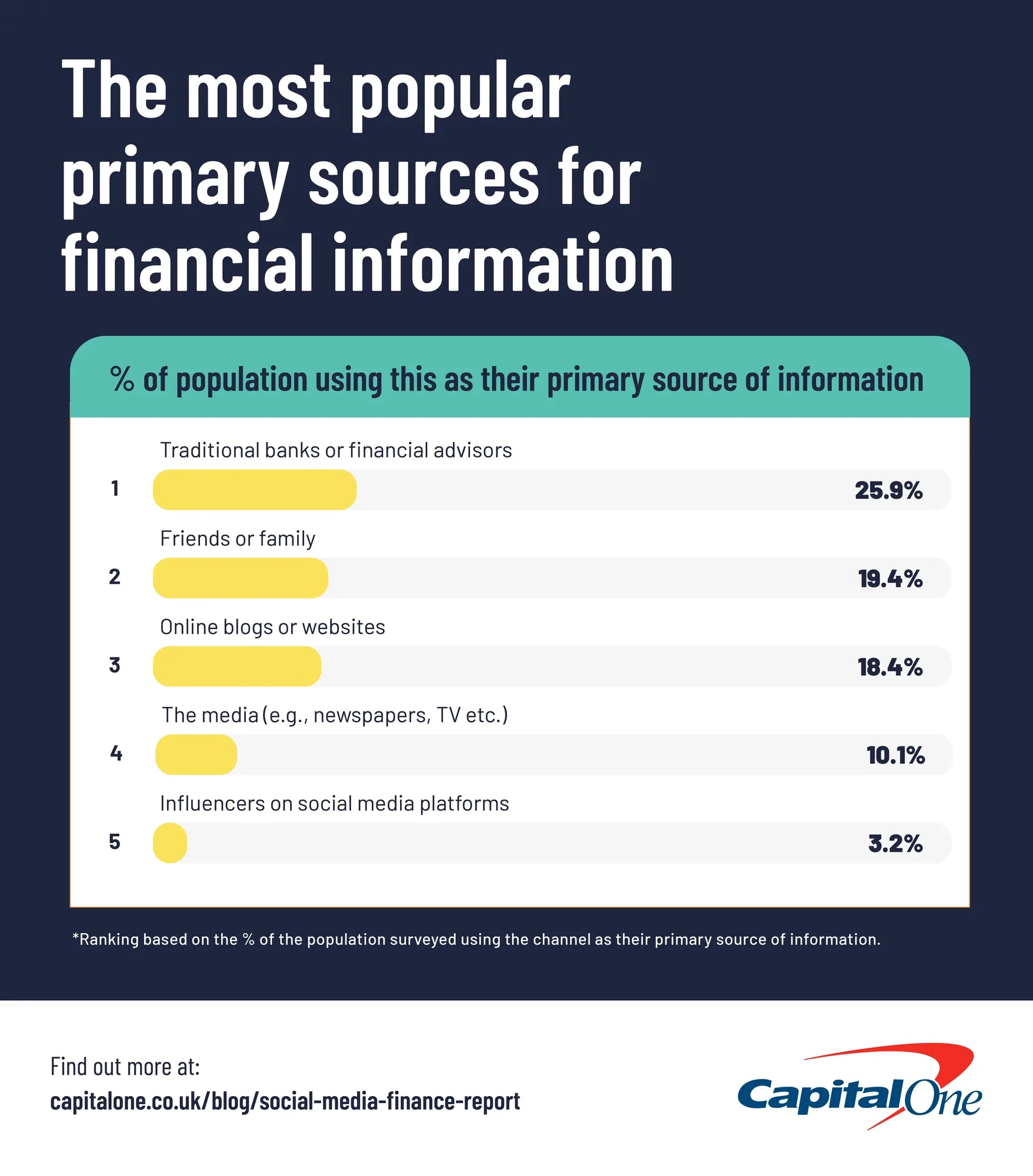

The most popular primary sources for financial information

| Rank | Source of Financial Information | % of Population Using This as Their Primary Source of Information |

|---|---|---|

| 1 | Traditional banks or financial advisors | 25.9% |

| 2 | Friends or family | 19.4% |

| 3 | Online blogs or websites | 18.4% |

| 4 | The media (e.g., newspapers, TV etc.) | 10.1% |

| 5 | Influencers on social media platforms | 3.2% |

*Ranking based on the % of the population surveyed using the channel as their primary source of information

Friends and family are one of the most popular sources for information

Unsurprisingly, traditional banks or financial advisors are the most popular source for financial guidance. Given that finance is such an important topic which can have a huge impact on people's lives, it's important to get information from experts where possible.

Following closely behind, friends and family are the next most popular primary source for financial information. Whilst this may be the easiest and most comfortable way to receive guidance, it's not always the best. Every financial situation is different and it's always important to get an expert's take on your situation to avoid doing anything that could impact your current financial situation negatively.

Media outlets are a preferred source of information to influencers

As we have discussed previously, people are using influencers the least primarily when they're looking for financial tips. Interestingly, media outlets are over three times more popular than social media with Brits looking to increase their financial knowledge.

This source is more popular with the older generations (55+). However, this is somewhat unsurprising as this demographic uses social media much less. For example, recent statistics show that just 12.9% of Facebook users fall into this age bracket, whereas 18-35-year-olds make up over 51% of users.2

What drives consumer trust for sources of financial guidance?

The credibility of the source is the most important factor for Brits looking to increase their financial knowledge

Out of all the options given in the survey, nearly half of the respondents cited the credibility of the source as the factor that would most influence trust when looking for any finance tips. This is followed closely by qualifications (in third), with over 30% identifying this as a signal of trust. This is somewhat reassuring that the majority of Brits are identifying these factors as trustworthy, given the impact bad financial guidance can have on someone's financial future.

Interestingly, previous personal experience is the second most popular factor that influences Brits, with over 36% of respondents citing this as something that would instil trust in the guidance. Whilst theoretically, it may seem to make sense to take guidance from someone who has been in a similar situation to you, every situation is unique regardless of its similarities. Therefore, to ensure you are getting the best financial guidance for you, make sure to see an expert.

The size of the platform is the least popular trust signal, but not with Gen-Z males

Following on from the discussion around influencers and social media being the least favoured platform for gaining financial knowledge, it's unsurprising that the size of the platform the guidance is coming from is the least trustworthy factor for trust. Despite this, Gen-Z males appear to disagree. 25.4% of respondents in this category cited that the size of the platform was one of the biggest signals of trust for them when it comes to financial guidance. Shockingly, this comes ahead of qualifications, one of the true signals of trust widely recognised for accurate financial guidance.

Financial literacy in the UK in 2023

Financial literacy is 'the ability to understand and effectively use various financial skills, including personal financial management, budgeting, and investing' according to Investopediaopens in a new tab. Having strong financial literacy can equip us to make good financial decisions and know how they could impact our futures.

In recent years we've seen financial literacy become an increasingly prevalent topic as platforms such as TikTok and YouTube make financial content more accessible. This is reflected in search demand with searches for the term on Google up 23% and by 25% on TikTok highlighting how more of us are actively looking to understand more about finance terms.

Within our research, we asked participants a series of questions on financial terms and challenged them to complete a test which analysed their level of financial understanding.

How much do people think they understand key financial terms?

| Rank | Financial Term | Respondents who claimed they slightly understood or fully understood the term |

|---|---|---|

| 1 | Interest rates | 85.9% |

| 2 | Mortgage | 83.5% |

| 3 | ISA (Individual Savings Account) | 83.2% |

| 4 | Inflation | 83.1% |

| 5 | Pension scheme | 76.8% |

| 6 | APR (Annual Percentage Rate) | 72.5% |

| 7 | Stocks and shares | 65.5% |

| 8 | Compound interest | 58.3% |

| 9 | Bonds | 55.2% |

| 10 | Mutual funds | 37.3% |

This part of the research investigated respondents' claimed understanding, asking their own opinion on the level of knowledge of key financial terms. According to the research, 'interest rates' was the term most people claimed they understood (85.9% of total) whilst 'mutual funds' was the least understood (37.3%).

Men claimed to have a better understanding of financial terms than women

When digging into the data further, the research uncovered that men felt they understood every term better than women did with an average. 77.1% of men claimed they understood each of the terms vs an average of 63.5% of women.

When looking regionally those in the East of England performed highest with an average of 73.1% of respondents in this area claiming a slight or full understanding of the 10 terms.

Which financial terms do people understand the best?

How do we score when tested on our understanding of financial terms? Whilst many of us may claim to understand financial terms when challenged with defining them we may find it more challenging than we initially thought.

| Rank | Question | Correct answer | % of correct responses |

|---|---|---|---|

| 1 | What are the benefits of an ISA (Individual Savings Account)? | Save or invest without paying tax on the interest, dividends, or capital gains | 71.6% |

| 2 | If the inflation rate is 3% for the year and your savings account gives you a return of 1%, how is the purchasing power of your savings affected? | Decreases | 63.6% |

| 3 | Which of the following best describes 'Net Worth'? | Value of assets minus liabilities | 61.2% |

| 4 | Regarding income tax brackets, if you move up to a higher bracket, how is your income taxed? | Only the income exceeding the threshold is taxed at the higher rate | 55.6% |

| 5 | What is 'Compound Interest'? | Interest that's earned or charged on top of existing interest and principle | 49.8% |

| 6 | With a 10% APR (Annual Percentage Rate) loan, what is true?

| Yearly loan cost, including interest & fees | 31.9% |

| 7 | If interest rates rise, what generally happens to bond prices? | Decrease | 15.6% |

Respondents performed best when asked about ISA accounts, with 71.6% giving the correct answer. When challenged with a question on bond prices only 15.6% of respondents gave the correct answer making it the term with the lowest level of understanding.

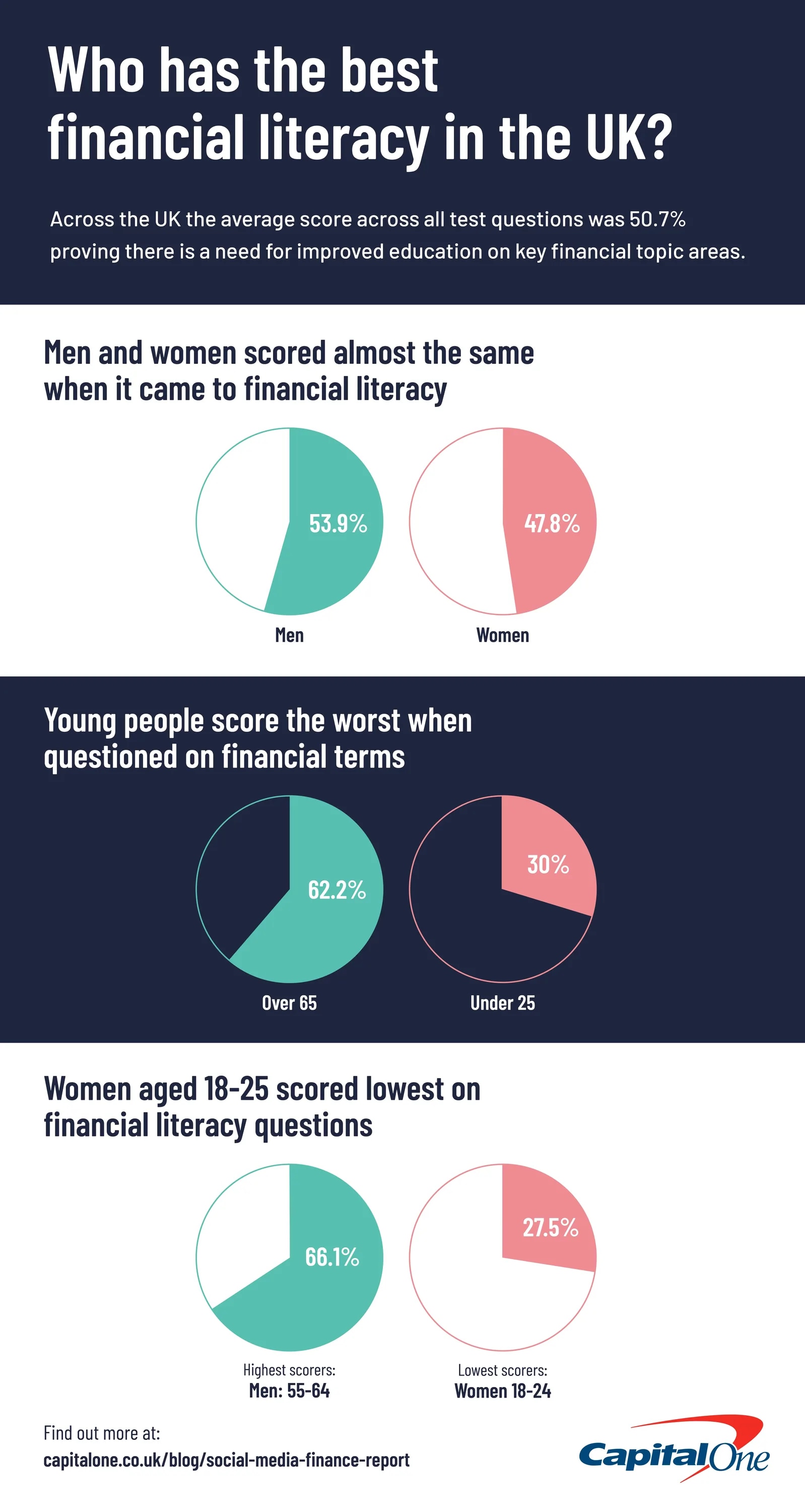

Who has the best financial literacy in the UK

When it came to financial literacy the level of understanding varied when analysed by age and location. Across the UK the average score across all test questions was 50.7% proving there is a need for improved education on key financial topic areas.

Men and women scored almost the same when it came to financial literacy

When analysing financial literacy by gender there wasn't a major difference between scores across those who identified as male (53.9%) and female (47.8%) with a gap of just over 6%. Both scored best on the ISA-related question and worst on the question regarding bond prices.

Young people score the worst when questioned on financial terms

On average respondents over the age of 65 scored highest in the financial literacy test with a score of 62.2% whilst those under the age of 25 scored on average just 30%. These results showed a large gap of understanding based on age, with the youngest people in the UK lacking the financial knowledge held by their elder counterparts, perhaps proving the argument that there is a greater need for financial education for young people in the UK.

Women aged 18-25 scored lowest on financial literacy questions

When combining demographics women in the UK aged 18-24 had the poorest level of financial literacy scoring 27.5% on average. The highest scorers were men aged 55-64 who scored on average 66.1% on the test.

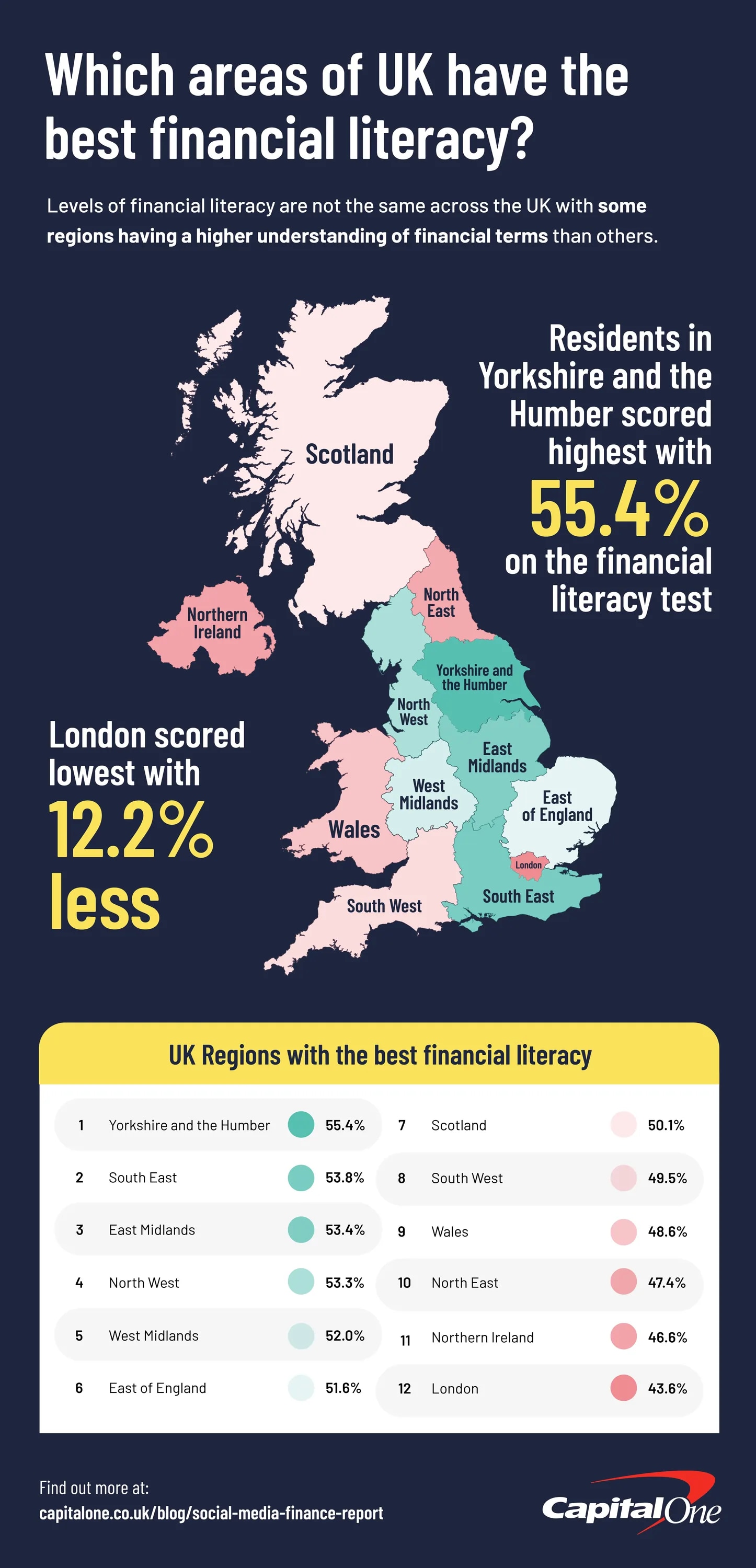

Which areas of the UK have the best financial literacy?

Levels of financial literacy are not the same across the UK with some regions having a higher understanding of financial terms than others.

| Rank | Region | Average Score |

|---|---|---|

1 | Yorkshire and the Humber | 55.4% |

2 | South East | 53.8% |

3 | East Midlands | 53.4% |

4 | North West | 53.3% |

5 | West Midlands | 52.0% |

6 | East of England | 51.6% |

7 | Scotland | 50.1% |

8 | South West | 49.5% |

9 | Wales | 48.6% |

10 | North East | 47.4% |

11 | Northern Ireland | 46.6% |

12 | London | 43.6% |

Residents in Yorkshire and the Humber have the best understanding of financial terms scoring 55.4% on the financial literacy test. Ranking last are residents in London who scored 12.2% less than the top-performing area.

Implications of financial guidance on social media

Do people's sources of financial guidance impact their level of financial literacy? With more of us using unregulated sources such as social media platforms and friends and family as sources of financial guidance it is important to consider if the guidance is influencing our own understanding of financial matters.

When combining the results from questions across the research we found correlations between the places where people get their guidance and how well they scored on the test.

Those who followed financial guidance on social media scored lowest when it came to financial literacy

| Rank | Source | Financial Literacy Test Score |

|---|---|---|

1 | Online blogs or websites | 60.57% |

2 | The media (e.g., newspapers, TV etc.) | 57.14% |

3 | Traditional banks or financial advisors | 54.47% |

4 | N/A - I don't seek financial information | 43.03% |

5 | Friends or family | 42.52% |

6 | Influencers on social media platforms | 28.12% |

Those seeing guidance from influencers on social media platforms scored lowest on the financial literacy test (28.12%) whilst those who got their guidance from online blogs or websites scored the highest (60.57%). Surprisingly, those who got their guidance from traditional banks or financial advisors scored 54.47% placing them only just higher than average, again putting into question the level of financial education available even for those who access regulated guidance.

Respondents who found influencers not very trustworthy have highest financial literacy

Further putting into question the quality of guidance being shared on social media the results showed that those who found influencers not very trustworthy scored the best on the test.

| How trustworthy do you find the financial guidance from social media platforms? | Financial literacy test score |

|---|---|

Not trustworthy at all | 19.05% |

Not very trustworthy | 45.30% |

Slightly trustworthy | 35.93% |

Very trustworthy | 29.30% |

The quality of financial advice on social media and video platforms

The increase in the volume of financial advice being shared on social media platforms is clear to see. TikTok videos with the #financialadvice have now been viewed over 323 million times whilst there are 33,830 searches a month on YouTube for keywords related to 'financial advice'.

Platforms are starting to provide better advice to users when viewing content of a financial nature. TikTok has introduced a disclaimer which automatically appears on content that is flagged as containing financial information which encourages users to 'Learn more about making informed financial decisions'. However, TikTok does not regulate content of this nature meaning anyone could create financial and share finance-related content.

Our research analysed YouTube videos containing key financial terms such as investing, credit cardsopens in a new tab and APRopens in a new tab to review the quality of financial content currently being shared on the platform. To do so we considered three key factors. We first analysed if the video contained any disclaimers within the descriptions which clearly outline the nature of the content e.g. someone without financial qualifications should provide a disclaimer that they aren't giving qualified financial information.

We then reviewed if the video or description included a disclaimer about affiliate marketing. Affiliate marketing allows creators to make money from their recommendations through using trackable links. Creators will usually get a commission when anyone who follows their link makes a purchase and as such this could influence their advice and the content within their videos and as such a disclaimer should be present.

Finally, we reviewed the creators of each video to find out if they had a financial qualification which could be clearly identified through their profile or online presence which would qualify them to give financial advice. Anyone without a qualification is giving financial advice or guidance without formal training or regulation.

The quality of financial advice on YouTube

Through analysing hundreds of videos on YouTube that contain content on financial topics we can reveal exactly how much of the advice available on the platform is of a high quality.

80% of financial content on YouTube is given by someone with no qualifications

Only 21% of all videos analysed were created by someone with a financial qualification (recognised by the Financial Conduct Authority to meet the requirement to provide financial advice) meaning almost 80% of financial content was not given by a financial advisor or someone with a relevant qualification. This highlights the risk taken when taking advice shared on the platform at face value.

Of the topics analysed videos on 'Savings' had the lowest number of qualified creators with just 9% of content on this being created by someone with qualifications.

Our research revealed that only 1.9% of financial content had all three crucial elements present meaning 98% of videos did not contain a disclaimer or outline their affiliate programs and their creator did not have a financial qualification.

Disclaimers were found in 50% of videos

50% of the content analysed did contain a disclaimer making it the element which was properly used in most videos. This still means however that half of the content shared on the platform did not include a disclaimer around financial advice.

Interestingly, only 28.1% of videos that shared information about financial advice included a disclaimer on this topic area.

Use of affiliates alongside financial advice

Only 6.2% of videos on financial advice contained a clear affiliate disclaimer. This could suggest that only a small percentage of creators in this area use affiliate schemes or could be that not all are clearly disclosing them.

Implications of unregulated financial guidance on social media

With our research showing that 13.7% of people are now looking at social media for financial information, this could mean over 5.4 million people are currently using social platforms as sources of financial guidance.

When analysing guidance on YouTube we found that up to 80% of content shared on the platform is done so by people without any financial qualifications which means millions of people could be using unregulated guidance to make financial decisions.

We also found a correlation between those who use social media as a source of guidance and a lower level of financial literacy, perhaps suggesting that the quality of content on social media is not good enough to empower people to make informed financial decisions.

Should we take financial guidance from social media?

Social media has opened up financial topics to millions of people making the finance industry much more accessible. Whilst there is lots of great guidance and content out there currently most social media platforms don't enforce any regulations when it comes to sharing financial information which in theory means anyone could create content that is positioned as financial guidance. As a result, it's important to not take the guidance you may see at face value without conducting research.

You should always consider whether to consult a qualified financial advisor before making any financial decisions and remember that financial products which involve investments always include an element of risk.

How to tell if financial guidance on social media is trustworthy

Things to consider before you follow financial guidance on social media

It can be confusing to decipher between financial content and financial advice on social media, however there are some factors to consider which can make identifying this much clearer.

Mr Money Jaropens in a new tab aka Timi Merriman-Johnson is a qualified financial advisor who provides accessible, practical financial guidance, through digital content, events and 1-2-1 coaching, and has appeared on the BBC, LadBible, ITV News, Sky News and Steph's Packed Lunch.

We asked him some questions on the topic of financial guidance and advice on social media so you know exactly what to look for when scrolling through your favourite social media apps.

What is the difference between financial information and financial advice on social media?

Guidance is non-prescriptive, will make the end user aware of their options and will highlight what they could do. Guidance is also generally free.

Advice is specific, personal, and will generally point to what you should do, and is typically (but not always) via a paid for service. It should therefore be pretty much impossible to give bespoke financial advice on social media, due to the large numbers of users involved.

How can I tell if financial advice I see on social media is genuine and if someone has a qualification to give it out?

You should generally not be receiving financial advice via social media, as the creator/ influencer will not have any access to specifics about you or your goals.

Qualified individuals will typically make this known in their social media names, handles or bios. Finance professionals who are linked to firms can also be searched on the FCA register, and the companies they are linked to.

How can I tell if financial content on social media is being sponsored?

All sponsored financial content on social media should clearly display the word or hashtag AD/ #AD in any post captions, story posts, tweets or livestreams, in accordance with ASA guidelines. The AD/ #AD identifier must also be visible above the fold, i.e., the user must not have to click 'read more' for it to be visible.

What are the benefits of watching finance related content on social media?

Finance related content on social media is accessible, available in bitesize chunks, and can react quickly to fast moving developments in the day to day world.

Because a content creator or influencer is likely to be the face of such content, it means that the end user is more likely to trust what is being said, as they will have developed an ongoing relationship with this person.

The creator may also be aware of any cultural, religious, societal or other relevant factors, which will make their messaging more appropriate for their audience(s).

Are there any actions consumers can take if they see misleading financial advice on social media?

- Consumers can report or flag any misleading information they see on social media to the social platform they are on

- Overt fraudulent activity can be reported to Action Fraud (the police)

- Misleading adverts or promotions can be reported to the Advertising Standards Authority (ASA) or the FCA

- Financial scams can also be reported to the Financial Ombudsman

What types of information should you always seek out a financial advisor for?

Suitable life milestones include:

- Buying a house

- Accessing your pension for the first time

- Getting married, divorced, widowed or starting a family

- When deciding what to do with a sizeable asset or lump sum

Methodology

Survey methodology

We surveyed 2000 adults representative of the UK population. The survey contained questions on financial guidance and where they source it from. The survey also included a 6 question financial literacy test designed to reveal participants' level of understanding of key financial terms and products.

Video analysis methodology

A total of 513 YouTube videos were analysed in total.

To gather the data for this video analysis, we put relevant keywords into YouTube's search engine to pull a list of URLs. This included:

- Credit Cards

- Financial Advice

- Save Money

- Money Making Ideas

- Side Hustles

- Credit Scores

- Financial Freedom

- Cash Stuffing

- Personal Finance

- Financial Planning

- Financial Investments

- Financial Goals

Transcripts for each video were then collected and analysed for the specific keywords used within the videos.

We then analysed whether the creator of the video disclosed affiliate programs or a financial advice disclaimer (e.g that they are not able to legally give financial advice and that the video is for educational purposes only) and if the creator had a relevant financial qualification.

We then used a combination of these elements being present or not to determine whether the content was reliable or not.

DISCLAIMER

This report should not be considered financial advice. Always consult a qualified financial advisor before making any financial decisions.